How to Budget When You’re Living Paycheck to Paycheck

Understanding the Paycheck-to-Paycheck Cycle

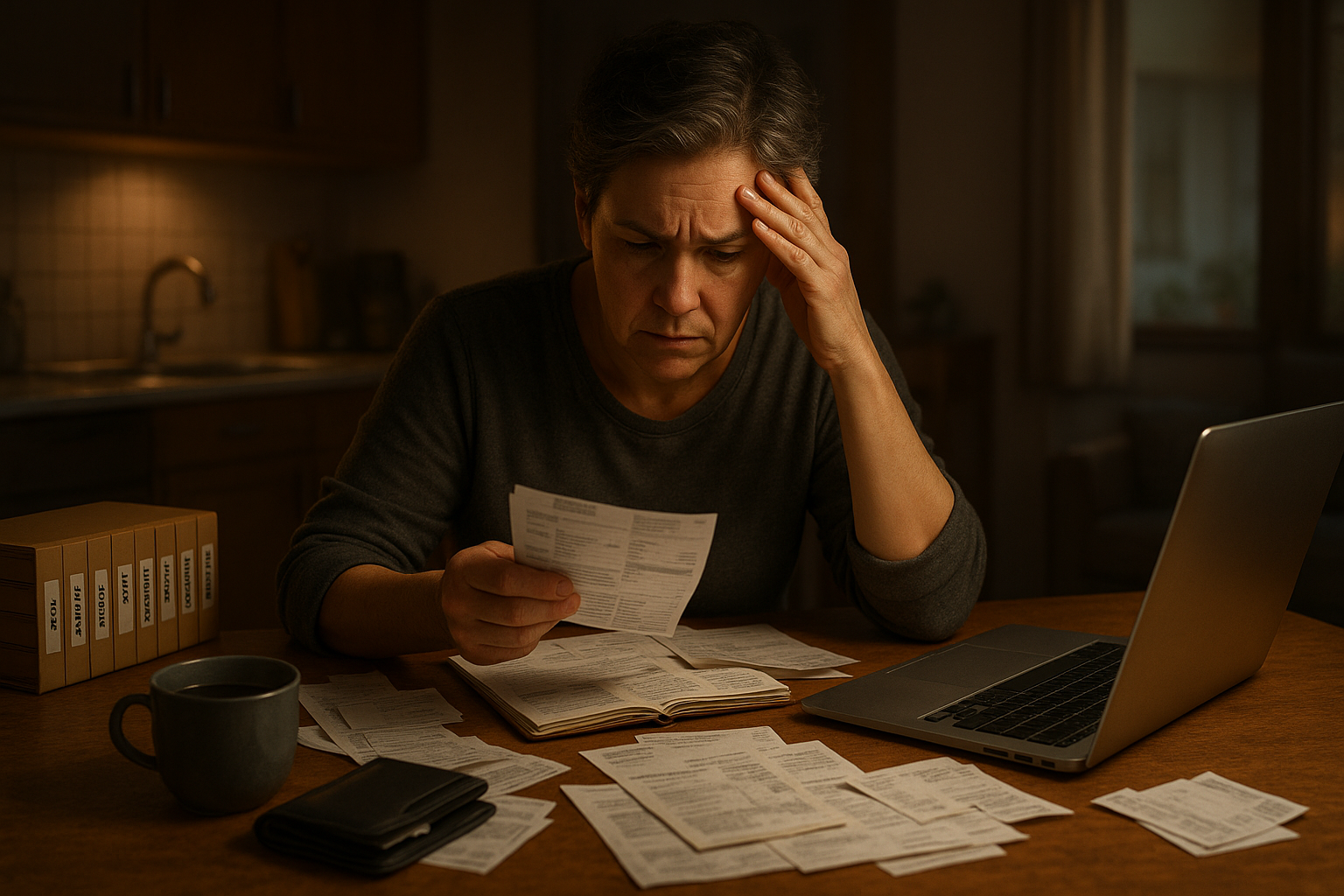

What It Really Means to Live Paycheck to Paycheck

Living paycheck to paycheck means your income barely covers your essential expenses. By the time rent, bills, groceries, and transportation are paid, there’s little or nothing left for savings or emergencies. It’s a cycle that traps millions of Americans, especially as inflation rises and wages stay stagnant.

The Emotional and Financial Toll of Constantly Starting Over

The pressure of constantly running out of money creates intense financial stress. It’s more than math—it’s the emotional weight of never feeling safe. According to a Forbes Advisor report, over 60% of Americans feel anxious about not making ends meet monthly. Budgeting becomes a form of survival.

Why Traditional Budgeting Often Fails in Tight Situations

The Problem with Generic Budget Advice

Standard budgeting advice—like “save 20% of your income” or “cut lattes”—misses the point when your income can’t cover basic living costs. The key isn’t to cut every luxury but to create a realistic system that reflects your unique constraints and goals.

Why Flexibility Is More Important Than Perfection

A budget that doesn’t bend breaks. You need flexibility to adjust for irregular expenses, small emergencies, and fluctuating income. This is where traditional spreadsheet-based budgeting often falls apart for people living on low income.

Step 1: Track Every Dollar (and Face the Numbers)

Know Exactly Where Your Money Goes

Before you can fix your finances, you have to face them. Start by tracking every single dollar over 30 days—no judgment, just awareness. Use budgeting apps like YNAB, Mint, or just a Google Sheet. Awareness is your first financial win.

Use Simple Tools or Apps to Help You Stay Aware

If spreadsheets feel overwhelming, try user-friendly tools like EveryDollar or PocketGuard. These help identify spending leaks and clarify your fixed vs. variable expenses.

Step 2: Prioritize Your Essentials

Start with Fixed Expenses and Survival Needs

Housing, utilities, groceries, and transportation come first. Then prioritize debt payments. If your income can’t cover all your bills, you may need to call creditors to request hardship plans or temporary deferments.

Build a Cushion for Emergencies — Even If It’s Small

Start an emergency fund—even $10 a paycheck counts. It helps break the debt cycle and prevents derailment when surprise costs hit. Consider opening a high-yield savings account or a cash envelope labeled “emergency.”

Step 3: Choose a Budgeting Method That Fits

Zero-Based Budgeting vs. Reverse Budgeting

Zero-based budgeting assigns every dollar a job so your income minus expenses equals zero. Reverse budgeting, on the other hand, pays yourself first (savings, essentials) and builds backwards. Test both and see what sticks.

Cash Envelopes, Apps, and Hybrid Systems

Visual learners often benefit from cash envelope systems. Others prefer the automation of digital apps. Many find success with a hybrid approach—automating bills, using envelopes for spending, and reviewing weekly.

Step 4: Automate Where You Can

Automate Bills, Savings, and Debt Repayments

Automating your essentials reduces decision fatigue. Set up autopay for fixed expenses and transfer $5–$25 per paycheck to savings automatically. This small act builds momentum and prevents overspending.

Reduce Decision Fatigue and Stick to the Plan

Each decision you eliminate gives you back willpower. Make savings and debt payments automatic, so you’re not re-deciding every month. It helps you build trust in your system and avoids forgetting key bills.

Step 5: Cut Costs with Strategy, Not Sacrifice

Target Discretionary Spending Without Feeling Deprived

Audit your subscriptions, dining out habits, and “just-in-case” purchases. Instead of eliminating joy, replace expensive habits with lower-cost alternatives—Netflix + homemade popcorn nights instead of $30 movie outings.

Cost-Cutting Ideas That Actually Work Long-Term

Use a meal plan to lower food waste, carpool or use public transit when possible, and negotiate service bills annually. These compound over time and preserve your financial dignity while trimming expenses.

Step 6: Rebuild Your Financial Mindset

Shifting from Guilt to Empowerment

Living paycheck to paycheck isn’t a failure—it’s a symptom of a broken system. You are doing your best with what you have. Shifting your mindset from shame to strategy helps you take aligned, confident action.

Set Tiny Wins That Build Confidence

Celebrate small milestones—paying off a utility bill on time, cooking at home three nights in a row, or saving $20 in a sinking fund. These wins compound both emotionally and financially.

What to Do When the Budget Still Doesn’t Work

Side Income, Community Resources, and Negotiating Bills

Consider taking on small side gigs, selling unused items, or using local food banks and assistance programs temporarily. Call utility companies or credit card providers to negotiate due dates and rates.

When to Seek Financial Counseling or Support

Organizations like NFCC offer free or low-cost counseling. You are not alone. Seeking support shows resilience, not weakness, especially when budgeting alone becomes overwhelming.

Conclusion: Budgeting Is Survival, Not Restriction

When you’re living paycheck to paycheck, budgeting becomes a form of protection—not punishment. By building a realistic, flexible, and emotionally sustainable budget, you regain control over your future. And with that control comes the space to breathe, dream, and eventually, grow.

FAQs

1. How do I start budgeting if I’m broke?

Start by tracking your spending and creating a zero-based budget. Focus on fixed expenses first and automate what you can.

2. What should I prioritize when budgeting with a tight income?

Always start with essentials like housing, utilities, and groceries. Then plan for debt, transportation, and small savings.

3. Can I still save money if I live paycheck to paycheck?

Yes. Even saving $5–$10 per paycheck builds the habit and creates a safety net over time.

4. What tools can help me manage a tight budget?

Apps like YNAB, EveryDollar, and PocketGuard help track spending and automate your plan.

5. What if budgeting still doesn’t work?

Explore increasing income, cutting deeper expenses, using local aid programs, or getting support from financial counselors.

Additional Resources

- Need a budgeting method that actually works? Read our Step-by-Step Budgeting Guide.

- Feeling overwhelmed by money stress? Learn how the psychology of money impacts your daily choices.

- Want to build an emergency fund with no room in the budget? Here’s how much you really need and how to start saving.

- For practical debt strategies, read Investopedia’s guide on zero-based budgeting.

- Learn more about financial counseling resources at the National Foundation for Credit Counseling.

- Track national income trends with data from the U.S. Census Bureau.